The American residential construction sector continues to grapple with a complex matrix of macroeconomic headwinds and sudden geopolitical instability, leaving industry executives with a guarded and cautious outlook for the remainder of the 2026 fiscal year. According to the latest data released by the National Association of Home Builders (NAHB) and Wells Fargo, the Housing Market Index (HMI) for March remained at a subpar reading of 38. While this figure represents a slight improvement over the historic lows seen during the summer of 2025, it signals that the majority of builders still view market conditions as "poor" rather than "good." The industry is currently caught between the competing forces of resilient buyer interest and a punishing cost environment, further exacerbated by a burgeoning conflict in the Middle East that threatens to disrupt global supply chains and energy prices.

The Stagnation of Builder Confidence

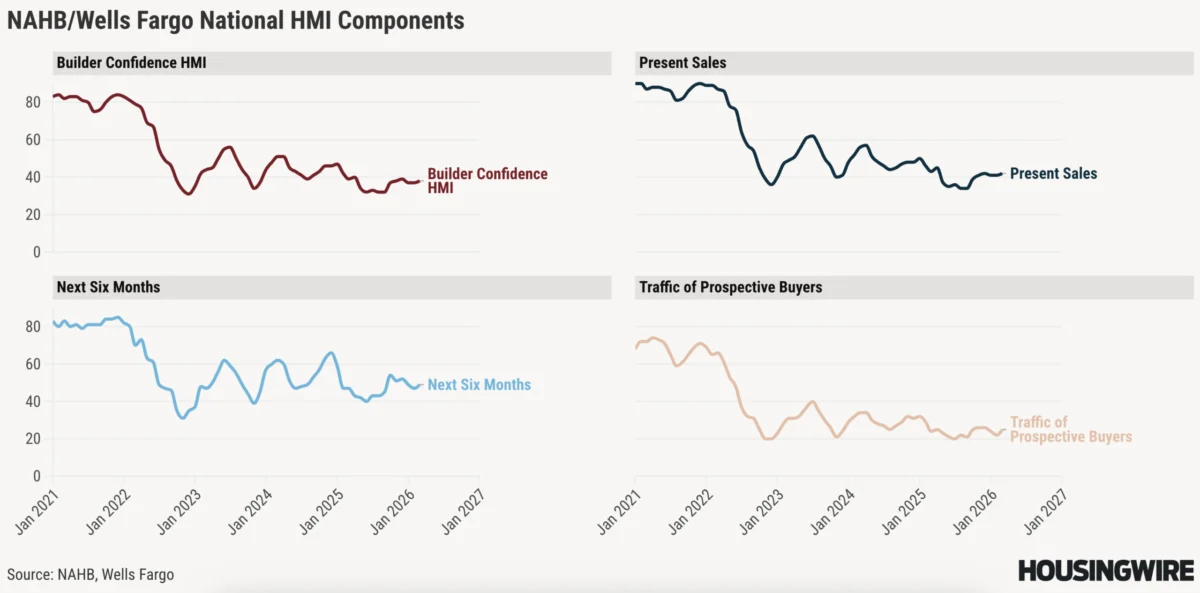

The HMI, a weighted average of three separate component scores—current sales, sales expectations for the next six months, and traffic of prospective buyers—has remained relatively stagnant since October 2025. A reading of 50 is considered the neutral midpoint; therefore, the current level of 38 indicates a significant contraction in optimism. Despite this, economists point out a "silver lining" in the trend line. Between June and September of the previous year, the index averaged a mere 32, suggesting that while the market is not yet thriving, it may have moved past its absolute nadir.

The persistence of low confidence is primarily attributed to three factors: tepid demand from price-sensitive consumers, shrinking profit margins due to high input costs, and a general erosion of consumer sentiment. Builders are finding it increasingly difficult to balance the necessity of selling inventory with the rising costs of production. As a result, the "wait-and-see" approach adopted by many potential homeowners has forced developers to engage in aggressive pricing strategies and marketing concessions to maintain sales velocity.

A Year of Incentives: The Strategy for Survival

The March HMI survey highlights the extent to which builders are relying on financial concessions to move units. For the 12th consecutive month, more than 60% of builders reported using sales incentives to entice buyers. Specifically, 64% of respondents offered some form of incentive in March, a figure that has remained remarkably consistent over the past year. These incentives often include mortgage rate buydowns, where the builder pays an upfront fee to lower the buyer’s interest rate for the first few years of the loan, or the inclusion of high-end upgrades at no additional cost.

Furthermore, 37% of builders reported lowering their base prices in March. While the average price reduction has stabilized at approximately 6%, the cumulative effect on profit margins is substantial. NAHB Chairman Bill Owens noted that affordability remains the primary hurdle for both the consumer and the developer. With buyers hesitant to commit due to economic uncertainty and the hope for lower interest rates in the future, builders are essentially "buying" their sales volume through these margin-eroding measures.

Geopolitical Disruptions: The Iran Conflict and Energy Spikes

The outlook for the US housing market was further complicated in early 2026 by the eruption of a significant military conflict involving Iran. The geopolitical tension has had an immediate and tangible impact on the domestic economy, primarily through the energy sector. The closure of the Strait of Hormuz, a vital artery for global oil shipments, has sent shockwaves through the commodities market. Crude oil prices, which sat at a manageable $65 per barrel prior to the escalation, have surged toward the $100 mark.

For the homebuilding industry, energy prices are a critical component of the "all-in" construction cost. High oil prices lead to increased transportation costs for heavy building materials such as lumber, steel, and concrete. Additionally, many building products, including PVC piping, roofing shingles, and various resins, are petroleum-based, meaning that a spike in oil prices leads directly to a spike in material costs.

The federal response to this crisis is currently in development. The Trump administration has signaled its intention to provide military escorts for commercial vessels through the Strait of Hormuz to ensure the flow of trade. Simultaneously, UK Prime Minister Keir Starmer recently emphasized that Britain is working in close coordination with international allies to reopen the shipping corridor. However, the lack of a definitive timeline for resolution continues to weigh heavily on market forecasts, adding a layer of volatility that builders are ill-equipped to manage.

Chronology of Market Shifts: 2025 to Present

To understand the current state of the market, one must look at the sequence of events leading into the spring selling season of 2026:

- Summer 2025: Single-family housing starts experienced a sharp decline of 7.3%, driven by peak interest rates and high inflation. Builder confidence hit a multi-year low of 32.

- Late 2025 (October–December): Mortgage rates began a slow descent from their peaks, leading to a modest recovery in the HMI to the mid-30s. Builders reported a slight uptick in "foot traffic" at model homes.

- January 2026: Single-family starts fell again by 2.8% to a seasonally adjusted annual rate of 935,000. However, multi-family construction saw a massive 29.1% surge, buoyed by the demand for rental units as homeownership became unaffordable for many.

- February 2026: The International Builders’ Show revealed a "cautious optimism" among insiders. Reports of improved sales paces in early February from major firms like Hovnanian Enterprises and Toll Brothers suggested the market might be bottoming out.

- March 2026: The escalation of the conflict with Iran and the resulting oil price spike dampened the early-year momentum. The HMI remained stuck at 38, reflecting new fears of "stagflation" within the housing sector.

Corporate Performance and Sector Divergence

The financial performance of public homebuilders provides a more nuanced view of the industry’s health. During recent earnings calls, several major players reported that demand has not evaporated entirely but has instead become highly sensitive to interest rate fluctuations. Hovnanian Enterprises, for instance, noted that its sales pace in January and the first half of February showed year-over-year improvement. Similarly, Toll Brothers reported a modest increase in deposits and traffic, suggesting that luxury buyers or those with significant equity are still active.

However, there is a stark divergence between single-family and multi-family sectors. While single-family starts have struggled, dropping 6.5% year-over-year in January, multi-family housing (buildings with five or more units) has shown remarkable resilience. The 29.1% month-over-month increase in multi-family starts in January indicates that developers are pivoting toward the rental market. As mortgage rates hover above 6.0% and the "downpayment hurdle" remains insurmountable for first-time buyers, the demand for high-quality rental housing has become a safer bet for institutional investors and developers.

The Mortgage Rate Dilemma

Mortgage rates remain the "X-factor" in the 2026 housing equation. In February, the Freddie Mac 30-year fixed-rate mortgage averaged 6.05%, which was the lowest level since August 2022. This brief window of relative affordability helped spur the traffic reported by Hovnanian and Toll Brothers. However, the onset of the Iran conflict and the subsequent inflationary pressure from energy costs have caused rates to tick back upward.

NAHB Chief Economist Robert Dietz has warned that these fluctuations create a "stop-and-go" economy for builders. When rates dip, buyers emerge; when rates rise due to geopolitical shocks, they retreat. Dietz forecasts that single-family housing starts will likely remain flat for the duration of 2026. He anticipates a more robust recovery of approximately 6% in 2027, provided that the geopolitical situation stabilizes and the Federal Reserve finds a path toward sustained rate reductions.

Labor and Land: The Permanent Headwinds

Beyond the immediate crisis in the Middle East, builders are facing structural challenges that predate the current conflict. The cost of labor remains elevated as the industry struggles with a chronic shortage of skilled tradespeople. Vocational gaps in plumbing, electrical work, and masonry have driven up wages, which are then passed on to the final price of the home.

Furthermore, the availability of "shovel-ready" land is at a premium. Stringent zoning laws and the rising cost of land development have made it difficult for builders to produce "entry-level" housing. This lack of affordable inventory is a primary reason why 64% of builders are forced to offer incentives; they are trying to bridge the gap between what it costs to build a home and what the average American family can afford to pay.

Analysis of Broader Implications

The current state of the homebuilding market serves as a bellwether for the broader US economy. Housing accounts for a significant portion of the Gross Domestic Product (GDP), and a prolonged slump in construction has ripple effects through the manufacturing, retail, and service sectors. If the Iran conflict persists and oil remains near $100 per barrel, the resulting "cost-push" inflation could force the Federal Reserve to keep interest rates higher for longer, further delaying the housing market’s recovery.

However, the resilience of the multi-family sector and the anecdotal reports of steady buyer traffic suggest that the underlying demand for housing remains strong. The US continues to face a structural housing deficit estimated in the millions of units. This suggests that the current slowdown is a matter of "affordability and timing" rather than a lack of fundamental need.

As the spring selling season progresses, the industry will be watching two key indicators: the stability of the Strait of Hormuz and the movement of the 10-year Treasury yield, which dictates mortgage rates. For now, the American homebuilder remains in a defensive crouch, navigating a landscape where geopolitical volatility and economic uncertainty have become the new status quo. The hope remains that 2026 will be remembered as the year the market found its floor, setting the stage for a more sustainable expansion in 2027.