The new Commercial Enhanced Data Program (CEDP) pricing structure implemented by Visa has officially gone live, with its profound financial ramifications now becoming evident on April statements. This monumental shift in interchange qualification rules and rates is proving to be an unwelcome development for a substantial segment of merchants, particularly those that process a high volume of Visa Small Business and Level II card transactions. The changes represent a complex recalibration of payment processing costs, demanding immediate attention and strategic adaptation from businesses across various sectors.

Understanding the Interplay of Interchange and Data Levels

To fully grasp the magnitude of Visa’s CEDP changes, it is essential to first understand the foundational concepts of interchange fees and data levels in card processing. Interchange fees are charges levied by card-issuing banks on acquiring banks for each credit or debit card transaction. These fees constitute the largest component of merchant processing costs and are set by the card networks like Visa and Mastercard. Historically, card networks have offered preferential interchange rates for transactions that include enhanced data, categorized as Level II and Level III.

Level I data typically includes basic transaction details such as merchant name, transaction amount, and date. Level II data adds sales tax and a customer reference number (like an invoice number), offering a slightly more detailed record. Level III data, the most comprehensive, provides extensive line-item detail, including product codes, descriptions, quantities, unit costs, shipping information, and tax breakdowns. The rationale behind these tiered rates has always been rooted in risk mitigation and reporting. Transactions with more data are generally considered less susceptible to fraud and provide richer reporting for corporate and government entities, justifying lower interchange fees. This structure has historically provided significant cost savings for businesses, especially those in the Business-to-Business (B2B) and Business-to-Government (B2G) sectors, which frequently handle large-ticket transactions using corporate, purchasing, and small business cards.

A Chronology of Shifting Policies: How CEDP Evolved

The journey to the current CEDP structure has been marked by a series of announcements and revisions from Visa, creating an evolving landscape for merchants.

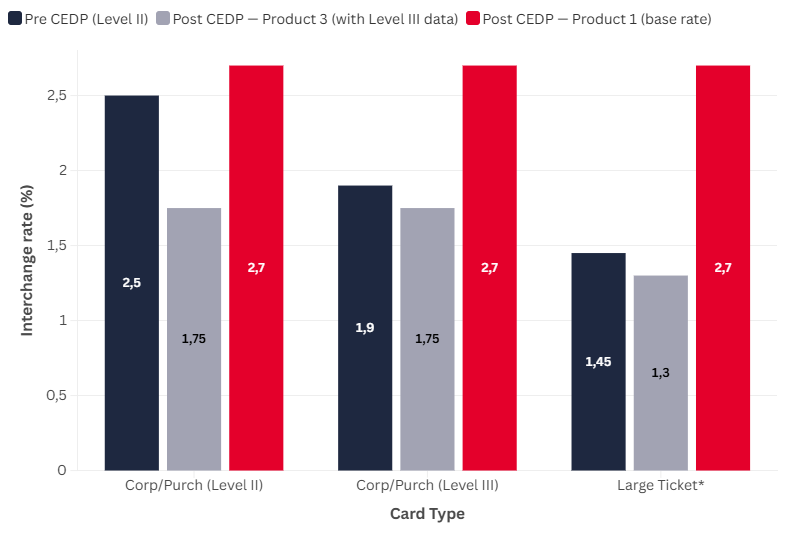

April 2025 – Initial Announcement and Promise: Visa first introduced CEDP with a seemingly straightforward and promising premise. Merchants processing Visa Small Business card transactions across Tiers 1 through 5, provided they submitted verified Level III data, would qualify for a new Product 3 interchange rate. The initial communication suggested this rate would offer genuine cost savings, surpassing the existing Level II rates. This announcement was met with cautious optimism, as it appeared to align with the industry’s push for enhanced data processing.

November 2025 – The Pivotal Revision: Just seven months after the initial announcement, Visa delivered a significant revision that fundamentally altered the program’s outlook. The proposed Product 3 rates for Small Business cards were slated to increase by a substantial 65 basis points. To put this into perspective, a basis point is one-hundredth of a percentage point. A 65 basis point increase translates to an additional 0.65% on every qualifying transaction, a considerable jump for any merchant, especially those with high transaction volumes. More critically, Visa announced the complete elimination of the Level II rate category for Small Business cards. This meant that these transactions would no longer have a Level II fallback option. Merchants would now face a binary choice: either qualify for the (now higher) Product 3 rate by successfully sending Level III data, or their transactions would default to the significantly higher Product 1 base rate. This revision fundamentally changed the program from a potential cost-saving initiative to a cost-mitigation challenge.

January 2026 – Implementation for Small Business Cards: The revised Product 3 rates for Small Business cards and the complete removal of their Level II category took effect. This date marked the first real-world impact for many merchants, who began to see an immediate uptick in processing costs for these specific card types. The financial statements for January and subsequent months started to reflect these changes, often without clear explanations for the underlying reasons, leading to confusion among businesses.

April 2026 – Broadening the Scope of Impact: Visa extended the retirement of Level II discounts to include Purchasing and Corporate cards. This added another layer of complexity and cost pressure for merchants processing these transaction types, which are common in B2B and B2G environments. While Fleet cards were temporarily spared, retaining a Level II category for the time being, the broader trend signaled a significant overhaul of commercial card interchange. This phased approach meant that merchants were hit with successive waves of rate adjustments, making it challenging to fully assess and adapt to the cumulative impact.

The Merchant’s Unenviable Dilemma: A Binary Choice with Varied Outcomes

The elimination of Level II rates for most commercial card types has presented affected merchants with a stark, binary choice: invest heavily in Level III data compliance or face substantially higher processing costs. However, the financial outcome of this choice varies dramatically depending on the specific card type.

Corporate and Purchasing Cards: A Challenging but Potentially Rewarding Path

For transactions involving Corporate and Purchasing cards, the transition to Product 3, despite the increased complexity, still represents a meaningful opportunity for cost savings compared to defaulting to Product 1. Merchants who are able to successfully invest in the necessary technology and operational processes to achieve consistent Level III data compliance can still realize rates that justify the effort. These cards are typically used by larger organizations with sophisticated accounting and procurement systems, which may be better equipped to handle the rigorous data requirements of Level III. The savings, while requiring upfront investment and ongoing diligence, can be substantial enough for these transactions to make the compliance effort worthwhile.

Small Business Cards (Tiers 1-5): A Losing Proposition for Many

The calculus for Small Business Tiers 1-5 cards is considerably more challenging, if not outright punitive, for many merchants. The new Product 3 rates for Small Business transactions are now significantly higher than what the Level II rates previously offered. This means that even merchants who successfully implement and maintain Level III data submission cannot fully recover the preferential rates they once enjoyed. They are doing exponentially more work—investing in systems, training staff, and monitoring transactions—only to achieve a rate that is still worse than their previous baseline.

For those merchants who are unable or unwilling to send Level III data for Small Business cards, the situation is even grimmer. Their transactions will default to the highest possible Product 1 base rate, representing a substantial and often prohibitive step up in cost. This segment of merchants, often smaller B2B providers or those with less sophisticated IT infrastructure, is caught between a rock and a hard place. They face either a costly and complex compliance burden for marginal benefit, or a significant increase in their operational expenses.

The Intensifying Burden of Compliance Complexity

One of the most significant, yet often underestimated, aspects of CEDP is the dramatic increase in compliance complexity. Under the legacy Level II program, merchants typically needed to provide only two additional data fields: sales tax and an invoice number. This was a relatively simple, sustainable, and scalable requirement for most businesses.

Under CEDP, qualifying for Product 3 necessitates numerous additional data fields. While the exact requirements can vary, they typically include:

- Customer Code

- Sales Tax Amount

- Freight/Shipping Amount

- Duty Amount

- Product Code for each line item

- Item Description for each line item

- Quantity for each line item

- Unit Cost for each line item

- Discount Amount (if applicable)

- Order Number

- Purchase Order Number

- Ship-From and Ship-To Zip Codes

Beyond merely submitting these fields, Visa’s verification systems actively scrutinize the accuracy and completeness of the submitted data. Merchants flagged for discrepancies, even minor ones, risk reclassification, meaning their transactions could be downgraded to the higher Product 1 rate. This transforms compliance from a one-time setup task into an ongoing, continuous monitoring requirement for every single transaction, indefinitely. The operational overhead involved in ensuring data accuracy across potentially thousands of transactions daily can be immense, requiring significant IT resources, process adjustments, and staff training. For Small Business card merchants, this translates to being asked to perform an exponentially greater amount of work for rates that are still inferior to their previous Level II savings.

Case Study: The $8 Million Invoice – A Tangible Impact

The impact of these changes is not theoretical; it is already being felt acutely by businesses. A large U.S. manufacturer, processing a significant volume of Visa Small Business card transactions across its diverse customer base, experienced an immediate and drastic financial hit. When Visa Small Business Tier 1-5 Level II rates were eliminated in January 2026, this merchant saw its annual card acceptance costs surge by approximately $8 million. This dramatic increase highlights how the new pricing structure, particularly the elimination of Level II for Small Business cards, can disproportionately affect high-volume merchants. The subsequent retirement of Level II for Purchasing and Corporate cards in April 2026 further exacerbated this financial pressure, adding to an already substantial burden. This case study serves as a stark warning to any company processing a high volume of Visa Small Business or Corporate card transactions, underscoring the potential for significant, and often unexpected, increases in their processing costs. Many merchants may not yet have fully reconciled their statements or understood the underlying reasons for these escalated expenses.

Visa’s Stated Rationale and Industry Reactions

While Visa has not issued specific public statements detailing the rationale behind the revisions to CEDP (especially the rate increases and Level II elimination), their general objectives for such programs typically revolve around:

- Enhancing Data Quality: Encouraging merchants to submit richer transaction data can improve fraud detection and provide more transparent reporting for commercial cardholders.

- Modernizing B2B Payments: Positioning Visa as a preferred network for complex B2B transactions by offering data-rich solutions.

- Streamlining Interchange Categories: Potentially reducing the number of complex interchange categories over time, although the current implementation appears to have added complexity for merchants.

However, the merchant community’s reaction has largely been one of frustration and concern. Industry analysts and merchant advocates have pointed out that while enhanced data is beneficial, the current CEDP structure imposes an disproportionate burden on merchants, effectively forcing them to absorb increased costs or invest heavily in compliance for diminishing returns, particularly for Small Business card transactions. There is a palpable sense among affected businesses that the promise of cost savings has been replaced by an unavoidable increase in operational expenses and transaction fees.

Broader Implications for the Payments Ecosystem

The implementation of CEDP carries significant implications that extend beyond individual merchants:

- Shift in B2B Payment Preferences: Faced with higher card processing costs, some merchants may increasingly encourage customers to use alternative payment methods like Automated Clearing House (ACH) transfers, wire transfers, or other electronic invoicing solutions, especially for large B2B transactions. This could lead to a subtle but significant shift in the B2B payments landscape.

- Impact on Supply Chains: Businesses operating within supply chains that rely heavily on commercial card payments, such as distributors, manufacturers, and wholesalers, will see their operational costs rise. These costs may ultimately be passed on to end-consumers or lead to tighter margins within the supply chain.

- Competitive Landscape: These changes could influence the strategies of other card networks. Mastercard, for instance, has its own enhanced data programs. The industry will be watching to see if similar adjustments are made by competing networks, potentially leading to a broader realignment of commercial card interchange fees.

- Technological Investment: The demand for Level III compliance will drive further investment in payment gateway technologies, enterprise resource planning (ERP) systems, and reconciliation tools that can automate the collection and submission of detailed transaction data. This presents both a challenge and an opportunity for payment technology providers.

- Small Business Burden: The disproportionate impact on Small Business card transactions raises concerns about the competitive viability of smaller B2B providers who may lack the resources to implement complex Level III compliance, potentially disadvantaging them against larger competitors.

Navigating the New Landscape: Strategies for Merchants

In light of these sweeping changes, merchants must proactively assess and adapt their payment processing strategies. Redbridge, a leading financial advisory firm, and other industry experts recommend several critical steps:

- Thorough Data Review: Conduct a comprehensive review of monthly interchange qualification and merchant statement data. This involves meticulously analyzing transaction-level detail to identify which transactions are being downgraded and why. Understanding the specific reasons for non-qualification (e.g., missing data fields, incorrect formatting) is the first step toward remediation.

- Assess CEDP Compliance Readiness: Evaluate current systems and processes to determine their capability for consistent Level III data submission. This includes assessing the payment gateway, ERP system, and any third-party integrations. Identify gaps in data collection, validation, and transmission.

- Build a Sustainable Monitoring Strategy: Compliance with CEDP is not a one-time fix. Merchants need to establish ongoing monitoring strategies to continuously verify that Level III data is being submitted accurately and completely for all eligible transactions. This may involve automated alerts for failed qualifications or regular audits of transaction data.

- Explore Offsetting Savings Opportunities: While CEDP presents new costs, merchants should also look for offsetting savings opportunities across the broader payments ecosystem. This could include renegotiating acquiring bank rates, optimizing other interchange categories, leveraging alternative payment methods where appropriate, or implementing new payment technologies that streamline operations and reduce overall costs.

- Engage with Experts: Partnering with payment consultants or advisory firms specializing in interchange optimization can provide invaluable guidance. These experts can help interpret complex interchange rules, identify specific qualification gaps, assist in system integration, and develop long-term strategies to secure and protect preferential interchange rates.

The rollout of Visa’s CEDP pricing structure marks a significant turning point in commercial card processing. While the stated aim may be to enhance data quality and streamline B2B payments, the immediate reality for many high-volume merchants is increased operational complexity and substantial cost escalations. Navigating this new landscape successfully will require diligence, strategic planning, and a proactive approach to payment optimization. Businesses that fail to adapt risk facing continuous erosion of their profit margins in an already competitive environment.