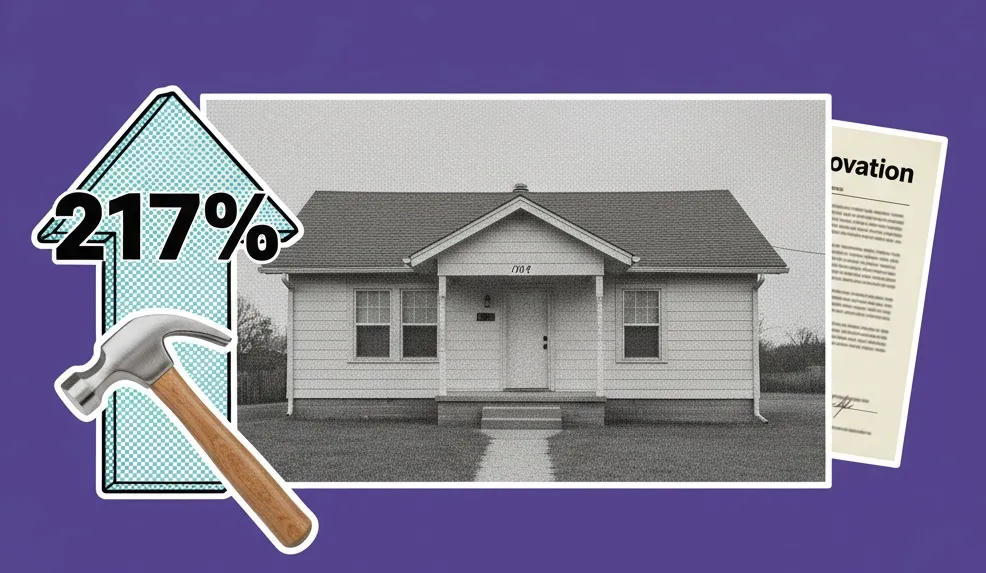

A fundamental shift in the American real estate landscape occurred throughout 2025 as small-scale, independent investors effectively bypassed traditional homebuilders to become the primary providers of entry-level housing. According to the 2026 Flip Side Report recently released by New Western, a leading private real estate marketplace, local investors delivered 120,193 homes in the starter-home segment during 2025. In contrast, traditional homebuilders supplied only 37,931 homes within the same price bracket. This disparity represents a 217% advantage for the investment sector over new construction, signaling a structural change in how affordable inventory is introduced to the market.

The report highlights a critical bottleneck in the U.S. housing market: the "starter-home" price point, typically defined as properties listed below $300,000. While the broader national conversation has long focused on the aggregate shortage of housing units, New Western’s findings suggest that the crisis is specifically concentrated at the entry point of the housing ladder. By revitalizing existing but distressed or vacant properties, small investors are filling a void left by large-scale developers who have increasingly pivoted toward higher-margin, luxury, or mid-tier residential projects.

A Statistical Shift in Housing Production

The 2025 data underscores a significant concentration of investor activity in the lowest price tiers. According to the New Western analysis, independent investors were responsible for 83.75% of all new housing inventory priced below $215,000. As the price point increases slightly, the investor share remains dominant; they accounted for 69.5% of the inventory available below $250,000.

Conversely, new construction has largely exited the entry-level market due to rising land costs, regulatory hurdles, and inflationary pressures on building materials. The report notes that just under 11% of all new homes constructed in 2025 were delivered within the starter-home price band of $261,000 or less. This suggests that for every one new home a builder creates for a first-time buyer, small investors are providing nearly three through the renovation of existing stock.

This trend is driven by the reality that many of the homes acquired by investors are invisible to the average consumer. Approximately 72% of the properties purchased by these investors in 2025 were never listed on the open market. These "off-market" homes were often in states of significant disrepair, making them ineligible for traditional financing and unattractive to the typical owner-occupant buyer. By intervening in this distressed segment, investors are effectively "recycling" housing stock that would otherwise remain uninhabitable.

The Chronology of the Entry-Level Shortage

The current imbalance between investor-led renovations and new construction is the result of a decade-long evolution in the real estate market. Following the 2008 financial crisis, homebuilders significantly scaled back production. As the economy recovered, builders focused on larger, more profitable homes to offset the rising costs of labor and land. By the early 2020s, the "missing middle" and "starter home" categories had become nearly extinct in the new construction sector.

The situation intensified in 2024 and 2025 as interest rates remained higher than the historical lows of the previous decade. This created a "lock-in effect," where existing homeowners with low-interest mortgages were reluctant to sell, further starving the market of entry-level inventory. In this environment, the only significant source of affordable housing became the distressed properties that required professional remediation—a niche that local, independent investors were uniquely positioned to fill.

Kurt Carlton, president and co-founder of New Western, characterized this movement as "The Great Renovation." He noted that the primary challenge facing the market is not necessarily a lack of physical structures, but rather a lack of "attainable" structures.

"What if the real housing crisis isn’t that we haven’t built enough homes, but that we’re letting millions of starter homes disappear?" Carlton stated in the report. "Fixing today’s housing challenge isn’t just about building more homes. It’s about whether attainable housing actually exists at the entry point. In 2025, small, local independent investors quietly became the largest suppliers of starter homes in America."

The Paradox of Vacancy Amidst Scarcity

One of the most striking findings in the report is the volume of underutilized housing stock in the United States. Data from the U.S. Census Bureau indicates that nearly one in 10 homes nationwide is currently vacant. Specifically, the analysis identifies more than 15 million vacant homes across the country. Additionally, there are an estimated 6.7 million occupied homes that require substantial repairs to meet modern safety and efficiency standards.

This surplus of "fixer-uppers" represents the primary raw material for the independent investor. While institutional investors (often referred to as "Wall Street landlords") frequently focus on purchasing move-in-ready homes to convert into rentals, the small-scale investors highlighted in the New Western report typically focus on the "fix-and-flip" or "fix-and-list" model. Their activity returns distressed assets to the owner-occupied market, thereby supporting the "first rung" of the housing ladder.

Regional Variations in Investor Dominance

The reliance on investors to supply starter homes is not uniform across the country; it is most pronounced in legacy markets with older housing stock. The report cites several metropolitan areas where the gap between investor activity and new construction is staggering:

- St. Louis, MO: In this market, small investors delivered 1,069% more starter homes than traditional builders. The city’s abundance of historic but neglected brick homes provides a massive inventory for local renovators.

- Boston, MA: Despite high overall property values, the entry-level segment in Boston saw investors supply 571% more homes than builders. In land-constrained markets like Boston, new construction is often prohibitively expensive, leaving renovation as the only viable path for creating "affordable" units.

- Atlanta, GA: Investors delivered 296% more starter homes than builders, reflecting the city’s rapid growth and the need for affordable options in the suburban periphery.

- Charlotte, NC: In one of the nation’s fastest-growing regions, investors outpaced builders by 149% in the entry-level segment.

These regional statistics suggest that in many of America’s most vital economic hubs, the traditional homebuilding industry has almost entirely ceded the sub-$300,000 market to private renovators.

Broader Economic and Professional Implications

The surge in investor activity has created a secondary economic engine within the housing sector. New Western estimates that the purchase and subsequent resale of investor-renovated properties generated more than $20.9 billion in listing agent commissions in 2025 alone. This activity supports a broad ecosystem of professionals, including real estate brokers, mortgage lenders, title companies, and local contractors.

For real estate agents, the findings suggest a need for a strategic pivot. As traditional inventory remains tight, renovated homes from local investors are becoming a larger share of the "move-in-ready" listings available to first-time buyers. Agents who cultivate relationships with local renovators are often better positioned to provide their clients with access to inventory that meets the "attainable" price criteria.

Furthermore, the "Great Renovation" has implications for neighborhood stabilization. By focusing on vacant or distressed properties, investors are not just providing housing; they are increasing local property tax bases and reducing the blight associated with long-term vacancies. The report argues that this "productive use" of existing stock is a more sustainable and immediate solution to the housing shortage than waiting for large-scale infrastructure and subdivision developments to clear regulatory hurdles.

Analysis of Future Market Trends

The dominance of the independent investor in the starter-home market is likely to persist as long as the cost of new construction remains high. Industry analysts suggest that until there is significant reform in zoning laws and a reduction in the "soft costs" of building—such as permit fees and environmental impact studies—homebuilders will continue to focus on the $400,000+ price range.

However, the investor-led model is not without its challenges. The rising cost of "hard money" loans and the increasing price of distressed assets themselves may eventually squeeze the margins for small investors. If the cost to acquire and renovate a home exceeds the $300,000 "starter" threshold, the supply of entry-level homes could contract even further.

For now, the 2026 Flip Side Report serves as a confirmation that the "mom-and-pop" investor has become an essential pillar of the American housing economy. By identifying and rehabilitating the millions of vacant and distressed homes scattered across the country, these individuals are providing the only viable entry point for a new generation of homeowners. The report concludes that without the 120,193 homes delivered by this sector in 2025, the national housing affordability crisis would be significantly more dire, with nearly 75% of the year’s entry-level inventory effectively non-existent.